After the 50/30/20 rule. Here is an advanced rule regarding budget management. The 45/20/35 Rule to optimize Financial Independence!

Recommended products

The rule 50 / 30 / 20

I explained in my article “ The rule 50 / 30 / 20 ”"that for a beginner in budget management regarding personal expenses. Good management would be to:"

- 50% mandatory expenditure

- 30% of pleasure expenses

- 20% savings and investment

In reality, this financial rule is an excellent starting point for managing your budget and improving your personal finances!

👉 However, I think this 50/30/20 rule is not suitable for the majority of frugal and minimalist readers of this site ⚠️

Mainly those who:

- Are accustomed to a frugal and minimalist lifestyle

- Have rather high incomes

Why is the 50/30/30 rule not suitable for frugalists?

Mainly for 2 reasons:

- 30% leisure is a high percentage

For example, if we calculate 30% from a net income of 5,000 CHF. That's 1,500 CHF of leisure per month.

Therefore, spending 1,500 CHF per month just for leisure activities is rarely frugal 🤭

Don't forget: the more you spend on leisure, the less money you automatically have to invest!

- 20% investment and savings rate is a low percentage for an investor

The majority of readers of this blog wish to achieve future financial independence (FIRE) and maximize the returns on their investments every month.

To achieve financial freedom, it is often imperative to invest larger amounts of money each month.

Therefore, taking into account the 50/30/20 rule1. The percentage of savings and investment is only 201%. This percentage is, in my opinion, rather low. 🔺

For example, out of the 20% of monthly investment, there are 15% for investments and 5% for savings.

👉 In this case, on a net salary of 5,000 CHF, 15% is “only” 750 CHF invested each month!

Let's imagine that there are 2,500 CHF of monthly mandatory expenses. Because the 50% of a salary of 5,000 CHF net is 2,500 CHF.

I went to moneyland's FIRE calculator. And I calculated the number of years to wait to become financially independent with:

- 2500 CHF of mandatory expenses per month, once FIRE

- Investment of 750 CHF per month until you become FIRE

- 5% annualized return on average, on the 750 CHF per month invested

In this case, the FIRE (financially independent) day will be in … 33 years 😶

Waiting 33 years to become FIRE is quite a long time 😶. Furthermore, this FIRE calculation only considers mandatory expenses.

We therefore conclude that to become financially independent, it is important to invest a larger share of one's income.

How to organize personal expenses to optimize financial independence?

➡️ We're reducing spending and increasing investment!

⚠️ I'm not saying it's obvious!

To make this change, you have to be disciplined and careful with your budget. But personally, I managed to do it with a low-mid income.

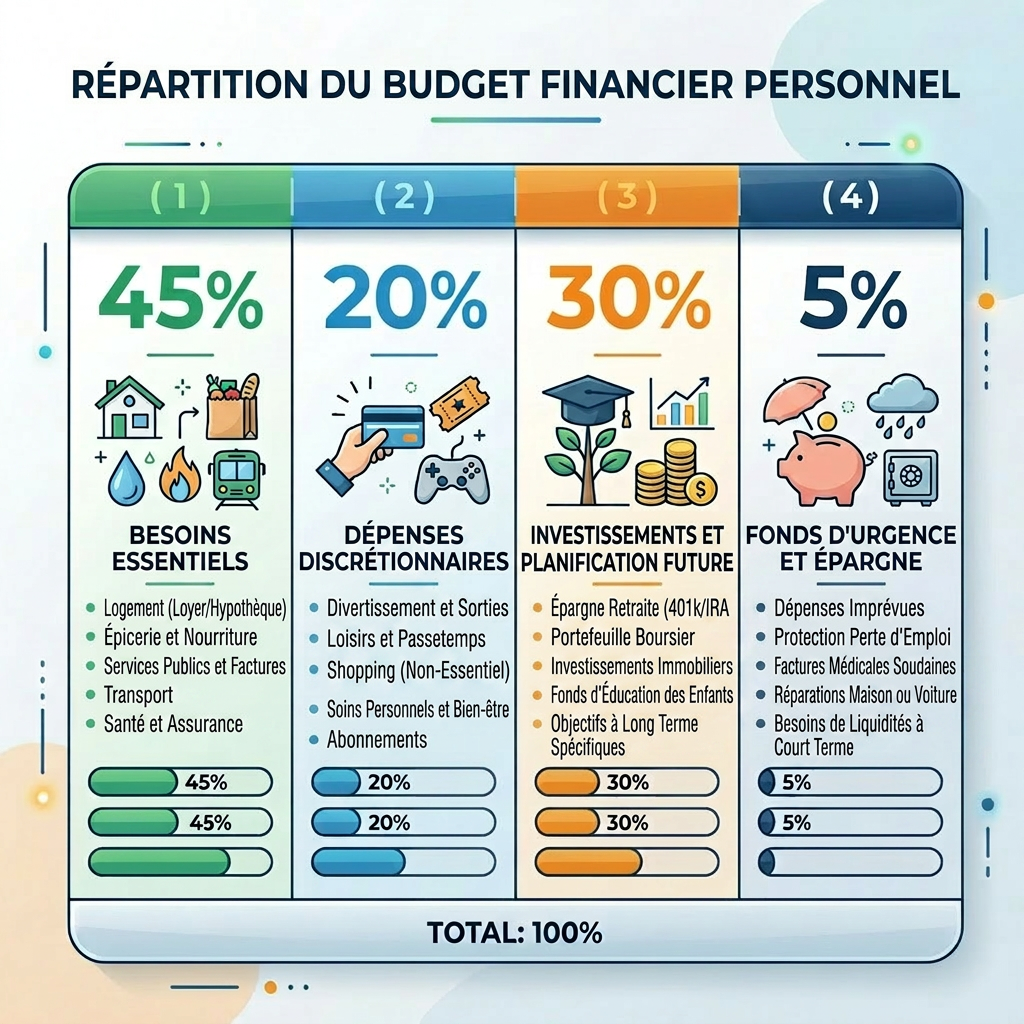

👉 In reality, I apply the 45/20/35 rule

Broadly speaking, I divide my budget between:

- 45% of mandatory expenses (of which a maximum of 20-25% is for housing)

- 20% pleasure spending

- 5% savings

- 30% investments

🔺Note that one of the best ways to achieve this rule is to apply each step on the page savings/frugalism from my blog 😊

I can guarantee that it's possible to live frugally and minimalistly on an average salary. Managing your budget isn't an impossible mission!

Also, my low consumption regularly makes me happy 😉.

Why prefer this 45/20/35 rule?

👉 To achieve financial freedom much faster 🤩

I'm using the FIRE Moneyland calculator again, with 45% in mandatory expenses and 30% in investments, and an annualized return of 5%. Financial freedom will be achieved in:

Hop! 12 years of financial freedom gained 😉

In fact, this rule allows you to become financially independent in less than 22 years!

Note that in the previous example, it took 33 years to become FIRE-compliant with 151 TP3T of investments and 501 TP3T of expenses. With 301 TP3T of investments and 451 TP3T of expenses, this is reduced to 21.5 years.

That's 11.5 years gained as a FIRE member 😉. That's not insignificant.

How to invest your money wisely?

Please note that this article is not investment advice. Investing involves risk of losing money.

In my opinion, with good knowledge, there are several financial investments to analyze. For example:

- Buying your main residence

- Investing in the stock market and buying growth ETFs

- Investing in physical real estate

- Owning SCPIs

- Owning a high-dividend equity ETF

In reality, every investor will need to analyze their investment portfolio so that it is diversified and profitable!

It should be noted that a good, regular return can allow for early retirement with a good standard of living and a prosperous financial situation.

Conclusion

➡️ Although the 50/30/20 rule is a great rule for beginners in personal finance. According to my In my opinion, this is too flexible a rule for people used to linking minimalism and frugality.

👉 If your personal finances allow, I think it's best to use the 45/20/35 rule to maximize financial independence and save money 😊

🔺Increasing investments boosts the chances of increasing passive income. Therefore, more income means fewer years depending on a client or boss 🤓

➡️ In my opinion, the 45/20/35 rule is more suitable for the majority of readers of this blog than the 50/30/20 rule.

45/20/35 Rule to Optimize Financial Independence!

FAQ – 45/20/35 Rule: Optimizing your budget for financial independence

What is the 45/20/35 rule?

The 45/20/35 rule is a budget management method that involves allocating one's income in this way:

- 45% mandatory expenses

- 20% pleasure expenses

- 35% savings and investment

The goal is to increase the savings rate in order to achieve financial independence more quickly.

Why is the 45/20/35 rule better than the 50/30/20 rule?

The 50/30/20 rule works well for beginners. However, for those who want to become financially independent more quickly, investing only 20% of their income may not be enough.

Reducing expenses and increasing the investment rate often accelerates the path to financial freedom.

What savings rate is needed to reach FIRE?

There is no universal figure. However, many followers of the FIRE movement seek to invest between 25% and 50% of their income in order to accelerate wealth accumulation.

Is it possible to save 35% of one's salary in Switzerland?

Yes, but this usually requires:

- strict budget control

- limited spending

- reasonable housing

- minimalist consumption

- little debt

High incomes in Switzerland also facilitate this objective.

How much do you need to invest each month to become financially independent?

The amount depends primarily on:

- the level of spending

- yield obtained

- existing heritage

- of the desired lifestyle

The higher the investment rate, the sooner financial independence can be achieved.

Where should the 35% of savings be invested?

It depends on the risk profile. Several solutions exist:

- Global ETFs

- account 3a invested

- real estate

- Dividend ETF

- main residence

Every investment carries a risk of loss.

Does minimalism help achieve financial freedom?

Yes. Minimalism often reduces:

- impulsive purchases

- fixed expenses

- the need to increase his income

Consuming less generally allows for more investment.

What is the maximum budget to allocate to housing?

In a frugal approach, many seek to keep housing below 25% of net income in order to preserve a strong savings capacity.

Does the 45/20/35 rule work with an average salary?

Yes. Even with an average salary, gradually increasing your savings rate can already produce significant results in the long term.

Can the 45/20/35 rule be changed?

Yes. This rule is primarily a framework. Some people prefer:

- 40 / 20 / 40

- 50 / 15 / 35

- 45 / 15 / 40

The important thing is to gradually increase the investment rate.

Subscribe for the latest news

You have a frugalist or minimalist project and you want a training? Click ”here”.

My pages

- About me

- Saving / Frugalism

- Blog

- Shop

- Contact

- Training and E-book

- Invest

- Minimalism

- My account

- Newsletter

- Basket

- Order confirmation

Lastest Post

- The 5 mistakes to avoid when starting out in the stock market

- How to invest in the stock market? The complete 7-step guide for beginners

- How does Inflation affect your wealth?

- How many years to achieve financial freedom?

- The 4% rule: The golden rule for financial independence

How does this blog live?

Overall, this blog lives on sharing a frugal and minimalist lifestyle.

For a question of transparency towards the readers. All recommended products are in order to make life cheaper, simpler and to promote the essentials.

Basically, my only income with this blog comes:

- Trainings that I realize

- Promo codes for the products I use

- Donations that readers make in exchange for neutral information.

About me

I decided to create this blog to develop and help readers who are looking for a simpler and more economical life.

Compared to before, I was a person who consumed a lot until the day I realized that my consumption made me sadder and poorer 😑

Now I prefer the minimum of my needs to be happy and achieve my financial freedom.

Without realizingI started to focus on saving and investing to depend on a boss for as little time as possible and to speed up my personal projects.

For several years I have felt happy and I have become richer in a way that I would never have imagined given that I have an average salary in Switzerland.

It is for this purpose that I decided to create this blog. In order to share and learn with other people who seek freedom and simplicity 😉

Are you rather minimalist or frugal Jonny?

I am as minimalist as I am frugalist. However, there are situations where I lean more towards an art of life.

To conclude, I think the most important thing is to feel comfortable in your lifestyle 😊

45/20/35 Rule to Optimize Financial Independence!

Leave a Reply