In this article, we're going to talk about a topic that comes up in the media every year: inflation! The main question is: how does inflation affect your wealth?

Recommended products

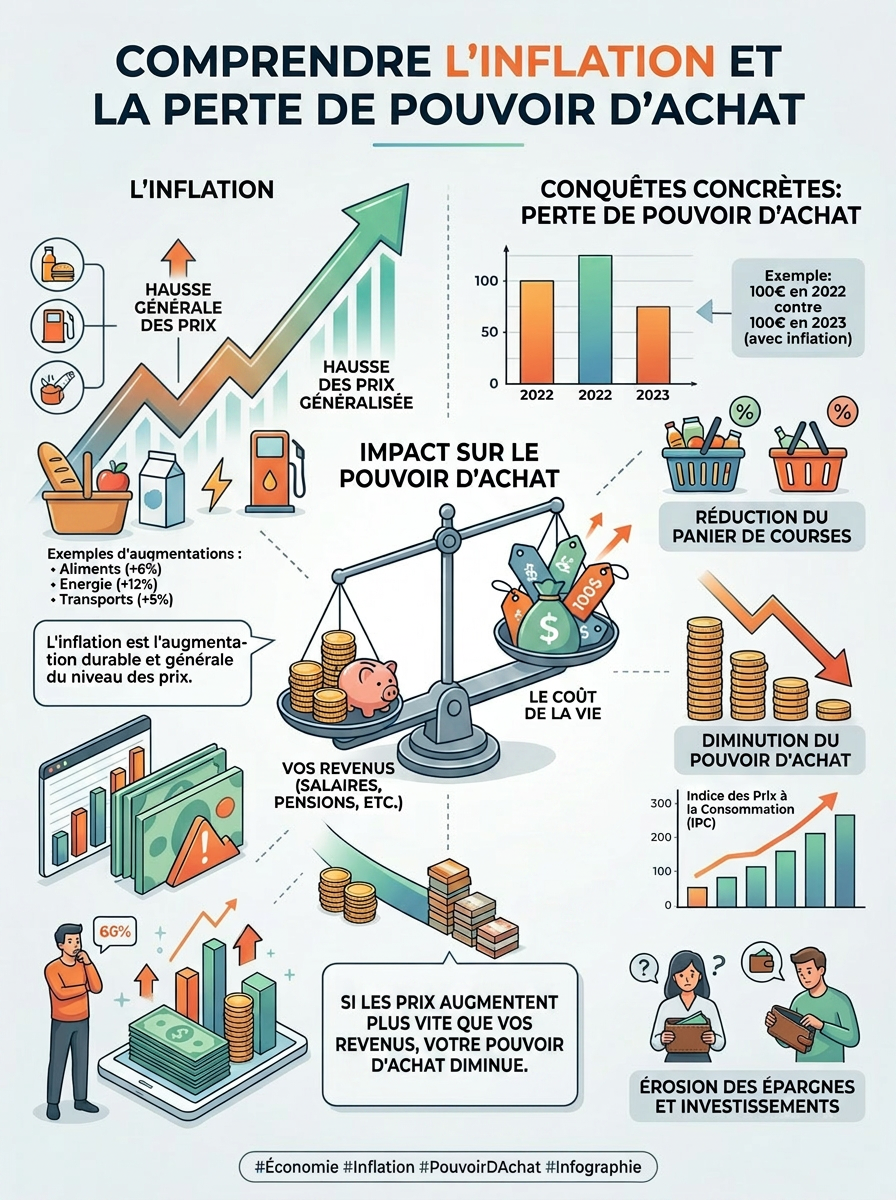

What is inflation?

👉 In summary, inflation is the change in prices for goods and services. If inflation increases, the cost of living rises. If it decreases, the cost of living falls.

▶ This is why inflation influences our purchasing power and influences our wealth. 🤔

When inflation rises, people talk more. That's normal; they're worried about the decline in their purchasing power.

Why are prices increasing?

There is no single cause of inflation. Several factors can cause prices to rise.

The most common ones are:

- an increase in production costs (energy, raw materials, transport…)

- a wage increase

- strong demand for a product or service

- a decrease in supply (bad harvests, shortages, conflicts…)

For example, if the price of oil increases, the cost of transportation also increases. Companies then pass on part of this increase to their prices.

Conversely, if wages increase in a sector, companies may also raise their prices to compensate for their costs.

👉 In reality, inflation is often the result of several phenomena occurring at the same time.

The history of inflation

Inflation is a normal phenomenon in an economy. Prices do not increase at the same rate every year, but over the long term, they tend to rise.

Using historical data from the last 30 years, we obtain approximately the following averages:

- Swiss : 1 to 2 % of inflation per year

- France: approximately 2 % of inflation per year

- UNITED STATES : 2.5 to 3 % of inflation per year

These figures are averages. In some years, inflation is close to 0%, or even negative. In other years, such as 2022, it can be significantly higher.

To make long-term financial projections, many people use an assumption of 2% of inflation per year. This is a simple, conservative estimate and close to the historical average for many developed countries.

In Switzerland, I think an inflation rate of 1.5% per year over the long term is a reasonable estimate.

Should we worry about inflation?

Definitely! But we shouldn't make a mountain out of a molehill either…

In my opinion, there is 5 essential aspects something to understand when we talk about inflation.

1. Average inflation is generally low in Switzerland

According to data from the Federal Statistical Office, inflation in Switzerland has remained relatively low in the long term. Between 2014 and 2023, it was approximately 1.1 % per year on average, which is significantly lower than that of many other countries.

For comparison, over the same period, France experienced higher average inflation, as did the United States.

That is why it is important to take a step back when we hear that a year shows an inflation of 0.5% or 1%.

In the long term, these variations are part of the normal functioning of the economy. Years in which inflation reaches several percent, as in 2022-2023 in many countries, remain more exceptional.

2. Average inflation doesn't necessarily reflect your daily life

Inflation is calculated from a basket of goods and services: food, energy, transport, housing, health, leisure, etc.

But everyone consumes differently.

For example :

- If you use your car a lot, the fuel price increase will affect you more.

- If you are a tenant, the increase in rents will be more significant for you.

- If you always cook at home, the increase in restaurant prices will hardly affect you.

👉 In other words, Your personal inflation may be very different from the average inflation reported in the media.

Therefore, it is often more useful to observe the price evolution of the products and services that you actually consume.

3. Inflation can vary by region

We often talk about a country's inflation, but prices don't necessarily evolve in the same way everywhere.

The cost of housing, transport or certain services may increase more rapidly in one region than in another.

👉 Two people living in the same country can therefore experience the effects of inflation differently, depending on where they live and their consumption habits.

4. Wages should ideally keep pace with inflation

Inflation is not a problem if your income increases at the same rate.

On the other hand, if prices increase faster than your salary for several years, your purchasing power decreases. That is to say, you can buy fewer goods and services with the same income.

In Switzerland, wages have generally increased over the years, but this does not mean that every employee has benefited from the same progress.

👉 That's why it's important to regularly check if your salary is at least keeping pace with the cost of living. Because if it isn't, you're losing purchasing power.

5. An inflation rate of 1-2% per year is not catastrophic

People often think that inflation is bad. In reality, a small amount of annual inflation is a good sign.

Inflation weak and stable (around 1-2 %) is generally considered healthy for an economy.

For what ?

- companies are investing more

- wages tend to increase

- consumers continue to buy

- The economy avoids deflation (which can be more problematic).

In reality, it is primarily very high inflations (5 %, 10 %, 20 %…) that become a concern, as this reduces household purchasing power, creates financial bankruptcies and strongly destabilizes the economy.

How does inflation impact your investments?

Inflation does not directly reduce the return on your portfolio. However, it does decrease the purchasing power of your money.

Let's take an example.

Let's imagine you spend 40,000 CHF per year

Let's also imagine that you've invested 40,000 CHF for a year.

At the end of the year, your portfolio shows a return of 8%.

Your capital is therefore worth: 43,200 CHF

You won 3,200 CHF.

But if, during that same year, inflation is 2%, Part of this performance simply serves to offset the general rise in prices.

Your actual yield is therefore: 8 % − 2 % = 6%

In the end, even if you have earned 3,200 CHF and you see +3,200 displayed on your account, in reality, your spending capacity is "only" 2,400 CHF.

In other words, your net worth has indeed increased, but your actual purchasing power has only increased by about 6%, and not 8%. That's inflation!

Example with 40,000 CHF spent per year

I went to an inflation calculator1. And I simulated an average inflation of 1.5% for 15 years. With annual expenses of 40,000 CHF.

A person who spends 40,000 CHF per year with an inflation rate of 1.51% per year will have to spend approximately 10,000 CHF more in 15 years for the same expenses. 😶

Why is inflation important for people aiming for FIRE?

Anyone who wants to become financially free must always take inflation into account.

For example, let's imagine you feel you need to 1,000,000 CHF to live off your investments.

If you achieve this goal in 25 years, 1,000,000 CHF will no longer have the same purchasing power as today..

This is why FIRE calculations use one of these two methods:

- 1) use a real yield, that is, a return after inflation.

They calculate the FIRE number by estimating future inflation, as in the example in the previous sub-chapter.

- 2) plan a higher FIRE number

They slightly increase the FIRE number. For example, if you spend 40,000 CHF per year, you multiply by 27 instead of 25 for the FIRE number.

👉 It's not the amount of your assets that matters, but what they will actually allow you to buy once FIRE.

How to avoid inflation?

In reality, it is impossible to completely avoid inflation.

However, it is entirely possible to limit its effects on your budget.

One solution is to adopt a more minimalist or frugal lifestyle.

👉 The more you reduce expenses that don't bring you much value, the less impact price increases will have on your finances.

For example, imagine that a brand of sugary drinks significantly increases its prices.

If you simply decide to stop buying them, this price increase no longer affects you.

In reality, reducing spending means limiting the impact of inflation.

The principle is the same for many discretionary expenses: restaurants, clothes, subscriptions, gadgets, etc.

⚠️ On the other hand, you will never be able to completely eliminate the impact of inflation, because some expenses remain essential (housing, food, energy, insurance…).

The goal is therefore not to avoid inflation, but to reduce the portion of your budget that is allocated to it.

Conclusion

Inflation is a normal part of an economy. In Switzerland, it has historically been low, but it still gradually reduces the purchasing power of your money.

The key is not to fear every variation in inflation, but to understand its impact on your personal finances.

In summary:

- Average inflation is different from your personal inflation

- Ideally, your salary should increase at least at the same rate as inflation, so as not to lose money.

- Investing for the long term helps preserve the purchasing power of your assets, even if part of your return will be eroded by inflation.

- Reducing or cutting expenses limits the impact of inflation; don't hesitate to spend only on essentials to minimize the impact of inflation on your wallet.

👉 Ultimately, the best way to protect your wealth is to combine good budget management with investments tailored to your goals.

FAQ: How does inflation affect your wealth?

What is inflation?

Inflation is the general increase in the prices of goods and services over time. When prices rise, your purchasing power decreases. That is, with the same amount of money, you can buy less.

What is the average inflation rate in Switzerland?

Over the last 30 years, inflation in Switzerland has been approximately 1 to 2 % per year, which makes it one of the developed countries with the lowest inflation.

What is the average inflation rate in France?

In the long term, inflation in France is close to 2 % per year. Some years may be much higher or lower, but this value represents a good historical average.

Why does inflation reduce purchasing power?

Because prices increase over time. If your salary or assets don't increase at the same rate, you can buy fewer goods and services than before.

How to protect your money against inflation?

The best solution is to invest a portion of your assets over the long term in investments capable of generating a return higher than inflation. Good budget management also helps to limit its impact.

Can inflation be completely avoided?

No. However, it is possible to limit its effects by reducing non-essential spending, avoiding overconsumption, and investing one's savings.

What is a good inflation rate for making financial projections?

To perform simulations over several years, many investors use an assumption of 2.% of inflation per year. For Switzerland, a hypothesis of 1,5 % is also consistent with historical data.

Is inflation always bad?

Not necessarily. Low and stable inflation is generally considered normal in an economy. It is primarily periods of high inflation that can significantly reduce household purchasing power.

How does Inflation affect your wealth?

Subscribe for the latest news

Do you have a frugalist project and would you like training? Click”here” and filled out the form

I suggest you read my tab”Frugalist” to read the main changes to save and become financially independent as quickly as possible.

My pages

- About me

- Saving / Frugalism

- Blog

- Shop

- Contact

- Training and E-book

- Invest

- Minimalism

- My account

- Newsletter

- Basket

- Order confirmation

Lastest Post

- The 5 mistakes to avoid when starting out in the stock market

- How to invest in the stock market? The complete 7-step guide for beginners

- How does Inflation affect your wealth?

- How many years to achieve financial freedom?

- The 4% rule: The golden rule for financial independence

How does this blog live?

Overall, this blog lives from sharing a frugal and/or minimalist lifestyle.

For the sake of transparency towards readers, all the products recommended are intended to make life cheaper and simpler.

Essentially, my only income from this blog comes from the training courses I conduct, promo codes for products I use, and donations readers make in exchange for neutral information.

About me

Faced with not very effective financial education, as was my case before. I actually decided to create this blog following a change in my life since my early adult life.

Compared to before, I was a person who consumed a lot until the day I understood that my consumption was making me sadder and poorer. From now on, I prioritize the minimum of my needs to be happy and achieve financial freedom.

Without realizing it, I also began to prioritize savings and investments to depend on a boss for as short a time as possible and to accelerate my personal projects.

For several years I have felt happy and I have become richer in a way that I would never have imagined given that I have an average salary in Switzerland.

It is for this purpose that I decided to create this blog. To share, learn and teach with others who seek freedom, simplicity and long-term wealth.

Are you rather minimalist or frugal Jonny?

I am both a minimalist and a frugalist. However, there are situations where I lean more towards an art of living.

To conclude, I think the most important thing is to feel comfortable in your life and I have found a balance between these lifestyles without reaching the extremes.

How does Inflation affect your wealth?

Leave a Reply